Someone had a question in a financial meetup group I attended today about where they should put a lump sum of money for future college expenses for their current 8th grader and 6th grader. Simplifying a bit, they are probably going to sell a rental real estate property and want to set aside the proceeds for possible college expenses. They are concerned about both current market conditions (high valuations) and current geopolitical risks, so are hesitant to invest it in the market right now. But they also realize that putting it in a money market account is not going to grow it a whole lot.

We had a robust discussion and a variety of opinions were expressed, including that despite the current high valuations and geopolitical events, no one can predict what the market will do (and that there is no strong correlation between those things and short-term market returns). We focused mainly on three (interacting) factors: time horizon, asset allocation, and asset location.

Time Horizon

Their children are likely four years and six years away from starting college (or other post-secondary options). But it’s important to realize that their investing time horizon is really four to ten years (at least), from when the first one starts to when the second one has completed four years (and, of course, it could be longer). Historically, once you get in the 5+ year time horizon, it makes sense to include a fair amount of equities (stocks) in your asset allocation. The problem is, of course, that for this person this is an N of one, so what has happened historically won’t be any consolation if stocks are down in this relatively short time frame.

Asset Allocation

So that then leads naturally into discussing asset allocation (as well as their risk tolerance). Given their legitimate concerns about market conditions and geopolitical factors, one option is simply to put it in a money market account, T-Bill, or other cash-like investment. Or, moving out the risk curve, they could invest some of it in short-term or medium-term bonds, or even include some equities in the mix. With a time horizon of 4-10 years, they also could “bucket” some of the money into lower risk investments (cash-like) and some into higher-risk (bonds and/or equities), on the assumption that for the younger one the time horizon of 6 to 10 years makes it very likely this will be a greater return than keeping it all in cash.

Asset Location

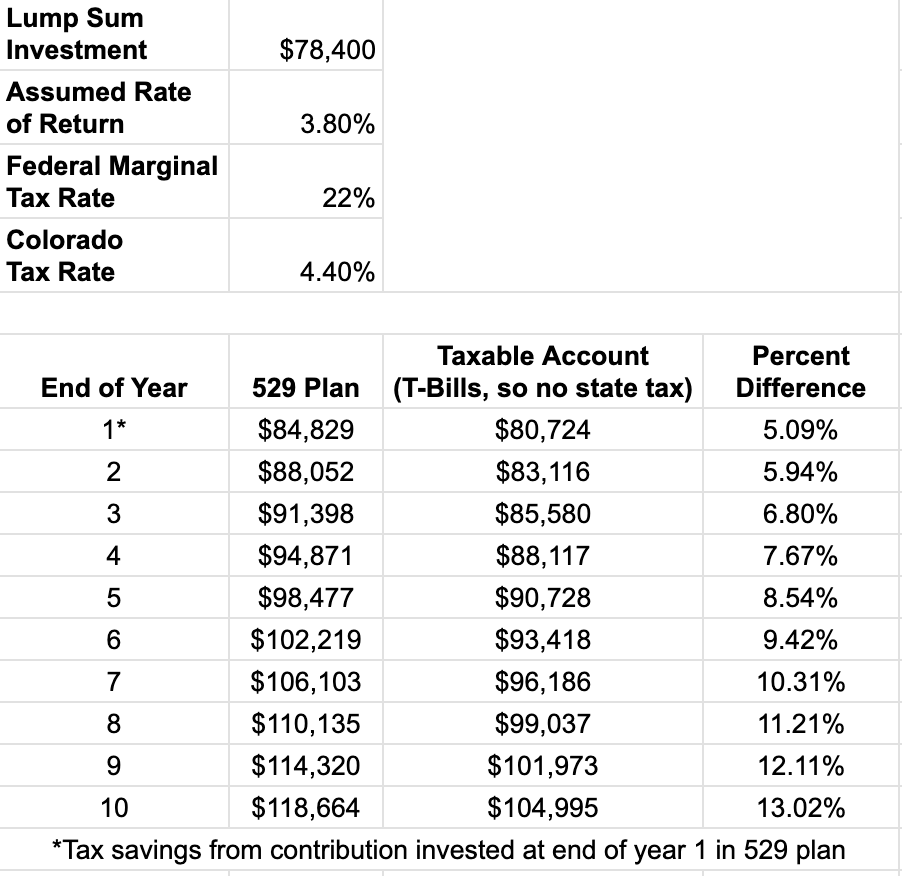

Then comes which type of account to invest this in, with the two choices discussed being a taxable brokerage account or a 529 account. This one is pretty much the reason for this post as I think it’s illustrative of the benefits of a 529 plan for many folks. I’ve written many times about Colorado’s 529 Plan, but the key point to know for this post is that in Colorado we can deduct contributions from our state income taxes (up to $39,200 per year for each beneficiary if married filing jointly; 2026 numbers). This means they could contribute up to $78,400 right away and get that state tax savings. That translates into an immediate (well, when they file their taxes, although they could immediately decrease their withholding) 4.4% return on investment (because Colorado has a flat 4.4% tax rate). But the tax savings continue, because any growth in the 529 plan is tax deferred and, if used for qualifying expenses, eventually tax free. Any growth in the taxable account would be subject to both federal and state income taxes along the way (tax drag).

So for the purposes of this example (and to keep it relatively simple), I decided to compare the results of investing a lump sum of $78,400 into cash-like investments in College Invest’s Direct Portfolio and in a taxable brokerage account like Vanguard or Fidelity. Like most 529 plans, College Invest’s Direct Portfolio has a variety of age-based options as well as static options. While we don’t know for sure how these will do over the next four to ten years, I think a return assumption of 3.8% (after fees) from the Income Portfolio is a reasonable expectation. If it was me, I would probably choose to be a bit more aggressive (and move “up” the risk curve in that list of investments) than that, and certainly would recommend that if they were starting this when the kids were younger. For the taxable brokerage account, I’m going to assume T-Bills as the cash-like investment because they will be exempt from Colorado’s state tax. Looking at current rates on 5-year and 7-year T-Bills, 3.8% also seems reasonable. (Yes, I’m artificially assuming the pre-tax return will be about the same in both accounts, but that seemed like the best way to compare.)

Here’s the spreadsheet (which you can choose File–>Make a Copy to get your own editable version to use whatever numbers you’d like). Here’s a screenshot.

I think this illustrates nicely the boost you get from the initial Colorado state tax savings on the contribution* as well as the advantages of not having the tax drag of the taxable account. Is it a humongous difference? No, but I still think it’s significant enough to choose the 529 plan.

Note the assumptions I used at the top (lump sum amount, rate of return, federal marginal tax bracket, Colorado tax rate).

If they wanted to contribute more than the $78,400 right off the bat they could, but they would only get the state tax deduction for the first $78.400. They could, of course, choose to contribute another $78,400 (plus whatever the increase for 2027 is) the following year to get the full tax deduction. Interestingly, because of the compounding effects from the tax savings, if you increase the assumed rate of return to something greater than 3.8% then the differences increase. (And, of course, if you choose something other than T-Bills that were not state-tax exempt, the differences would also be greater.)

This doesn’t mean that a 529 plan is right for everyone, or that this is the right asset allocation for short-term money. But it was designed to illustrate the advantages the state tax deduction for contributions as well as the tax-free growth provide you even over a relatively short-term time horizon. And this applies to even shorter time horizons, for example if you need to pay tuition next month. You can contribute money to the 529 plan today, and then a few days later you can withdraw it and still get the state tax deduction (it takes them a few days to process, so probably give yourself at least a week). So even if you can’t leave it in there very long at all to grow, it can still be worthwhile just to get the 4.4% discount on college expenses.

*In the spreadsheet I assume the tax savings from being able to deduct the contribution is invested into the 529 plan at the end of year one. In reality it likely would be invested a bit sooner than that and, in fact you’d get to deduct that contribution as well on the next year’s taxes, but the spreadsheet keeps it simple.