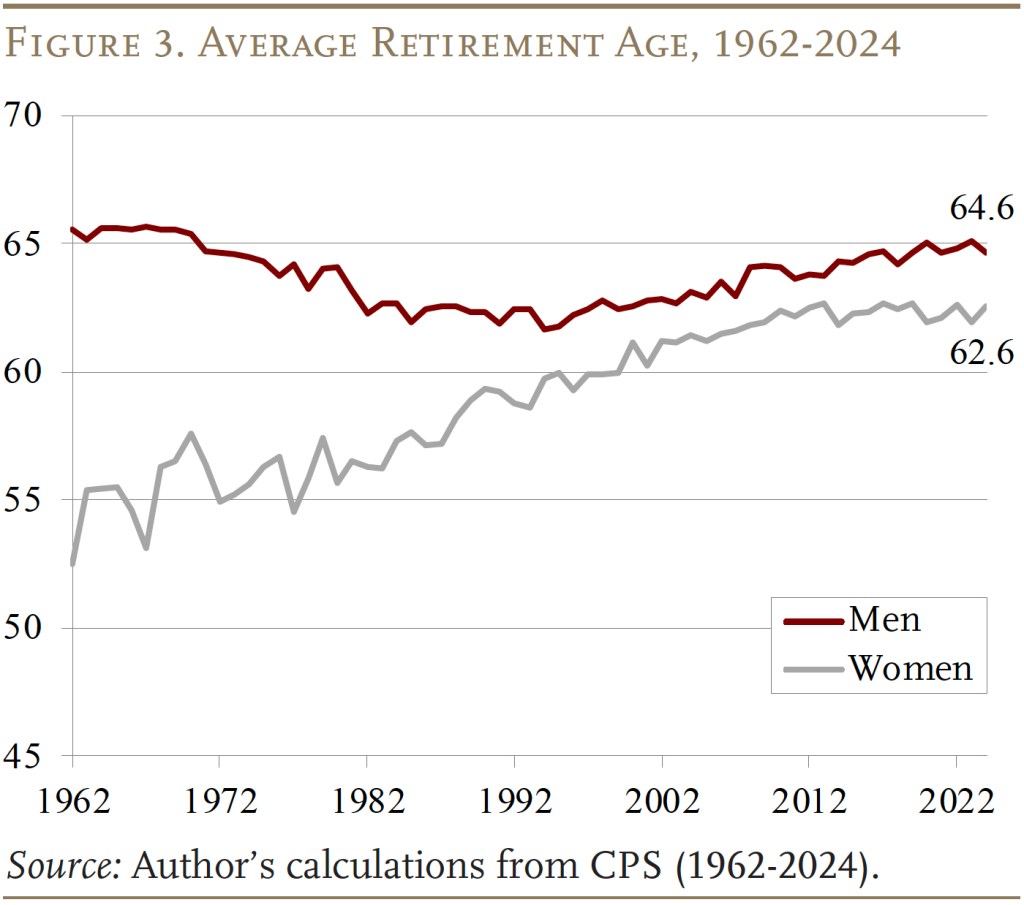

As I’m preparing for the Educational Session on Tax Planning, Safe Withdrawal Rates, and Withdrawal Sessions on May 2nd, I’m reminded of some factors that act as tailwinds for folks who retire a bit earlier than average. Before we talk about those tailwinds, we need to define what “average” is. The latest data I’ve seen indicate that the average retirement age for men in the United States is 64.6 and for women it’s 62.6 (and of course the Full Retirement Age for Social Security is now 67). Interestingly the average age seems to vary pretty significantly by state. For the purposes of this post, I’m going to define early(ier) as age 60 or younger.

When discussing early(ier) retirement with folks, whether it’s people who are trying to retire really early (like in their 40s) or people who are retiring moderately early (like mid to late 50s), I’ve noticed that many of them tend to focus on the possible negative events that can derail their plans in retirement. These events include a big market downturn, a more general sequence of return risk early in retirement, the cost of health insurance, medical bills and/or possible long-term care, and high inflation (to name a few). And, to be clear, these are real concerns and need to be part of your planning process. If you ignore these factors when determining when you have “enough” to retire and live the lifestyle you want in retirement you could end up having your lifestyle severely curtailed if and when they happen.

But there’s also a flip-side to these concerns that many early(ier) retirees tend to discount or ignore completely. You might call them “white swans” or simply “tailwinds.” The following list is not exhaustive, but these are some of the tailwinds that I find many people discount or ignore.

Social Security and/or Pension

Lots of people seem to think they can’t “count on Social Security still being there” by the time they reach the age of eligibility (currently sometime between age 62 to 70 for most folks). I don’t share that concern. I think at worst benefits might be a little bit lower than they currently are or they might start at a little bit later age than they currently do. But the default assumption should still be that you will get what the current formula tells you and you will get it within the current range of ages. The average Social Security benefit is currently $2,071 a month. For folks who are retiring early(ier), their benefit could be a bit below average (because their 35 highest years of earnings may be lower than someone who continues to work into their 60s). But it might not be, because many early(ier) retirees have had higher incomes and/or will be able to delay their benefit until age 70 (and get the “raise” by delaying the start date of their benefits). Let’s assume it will be “only” $1,500 a month for our early retiree. That’s $18,000 a year (partially tax exempt at the federal level, and often completely tax exempt at the state level). And if they have a partner you can double that. Using the “4% rule of thumb”, that’s equivalent to suddenly adding $900,000 to your investments sometime between age 62 and 70 – except there is no chance you’ll exhaust it. That’s a significant tailwind that can help “replenish” your retirement accounts that you’ve spent down in early(ier) retirement.

People who know they are going to get a defined-benefit pension are typically more confident that they will get it than folks with Social Security. Often these folks are retiring early(ier) at the point they are eligible to start drawing their pension, so it’s part of their planning process. But many folks haven’t thought about retiring before they are eligible to start drawing their pension and then “aging in” to their pension benefit. There are many people who might be able to retire earlier than they thought, even without their pension kicking in, if they then factor that their pension will kick in (perhaps at age 60 or 65 depending on their years of service and what benefit tier they are on). Looking at Colorado PERA, the average pension benefit is currently $3,264/month. Again, someone who is retiring early(ier) might have a lower (eventual) benefit, so let’s go with $2,500/month. That’s $30,000 a year, and again you could double that for a partner who also has a pension, or add in the $18,000 from above if your partner has Social Security (and pensions are often partially tax-exempt in many states). Using the “4% rule of thumb”, that’s like adding $1.5 million to your portfolio sometime in your 50s or 60s – except there is no chance you’ll exhaust it. Once again, this is a big tailwind for an early(ier) retiree. (And, for folks with non-covered pensions, the passage of the Social Security Fairness Act means you’ll likely get an extra, bonus tailwind.)

Inheritance

People really don’t like to think or talk about this. And, obviously, it doesn’t apply to everyone. But for many, many folks, an inheritance from their parents (or extended relatives) is in the cards. There is an estimated over $80 trillion getting passed down over the next 20 or so years. While you don’t know what end of life expenses might look like, and those could definitely lower the inheritance amount (as could other spending and/or market downturns), many people should be expecting a pretty significant “lump sum” boost to their finances, typically in their late 50s to late 60s. While you don’t want to write those numbers in ink in your plan, you should definitely pencil them in as a probable tailwind, another factor that may lower the “number” you need in order to feel comfortable retiring. (As an aside, this book is an excellent resource to help you have conversations with your parents.)

The Spending Smile

While every person’s retirement is unique, we can learn from the aggregate experience of all retirees. And what the research shows it that spending in retirement resembles a “smile”. This is also sometimes referred to as the “go-go” years, followed by the “slow-go” years, followed by the “no-go” years. For most (but not all) retirees, spending in retirement is the highest at the beginning (during the “go-go” years), then gradually declines throughout retirement, and then sometimes with an increase right at the end due to medical bills and long-term care expenses. What this means is that many people may be able to retire sooner than they think, because their initial “safe withdrawal rate” can perhaps be higher than what the simple math tells them, because their spending (and therefore their subsequent withdrawal rates) will gradually decline. This is especially true if you factor in all of the other tailwinds mentioned in this post, as well as the fact that any increase in spending at the end of life is likely short term (and typically has a definite end date, eliminating longevity risk in those last few years).

Update 3-24-26: This video does a good job of updating the spending smile research and explains that the uptick in late retirement spending is typically very modest.

Medicare

Health insurance premiums as well as out-of-pocket costs are a significant factor in retirement. But you can also plan on a significant decrease in both of those when you turn 65 and Medicare kicks in. Both your premiums and your out-of-pocket costs will drop dramatically. This is likely occurring at about the same time as other tailwinds; Social Security or Pension, inheritance, and getting close to the decrease from the spending smile kicking in. Again, people focus on having “enough” to meet their initial spending needs, but then they often project those spending needs out indefinitely, when the reality is that multiple tailwinds will either increase their income or lower their spending later in retirement.

Inflation and Investment Returns

Inflation is high on the list of concerns of anyone considering retiring early(ier). And it should be, as the compounding effects of inflation are real and significant (especially if you happen to experience higher-than-normal inflation in the first few years of retirement). But folks tend to ignore a few crucial factors. Assuming you have a decent amount of investments in a low-cost, diversified portfolio of index funds. your investments have historically outpaced inflation over time. This is one of the major reasons the “4% rule of thumb” has been so successful. In the majority of historical 30-year retirement time frames, people end up with a balance in their investment accounts that is greater than what they started with. There’s obviously no guarantee of this, but I think many people unconsciously project a linear decrease in their investment accounts over time based on their withdrawal amounts. That is unlikely to be the case.

This is the point where some folks will raise sequence of return risk. Again, this is a legitimate concern and something you need to factor in. But people rarely think about the “white swan” of a positive sequence of return risk. Yes, a negative sequence of returns early in retirement (generally the first 5-10 years of early(ier) retirement) can throw a big wrench in your retirement plans (and the assumptions you initially made about a safe withdrawal rate). But it’s just as likely that you’ll have a positive sequence of return risk, which will dramatically increase what you can withdraw early(ier) in retirement. Because humans are loss-averse, we tend to discount or completely ignore this possible tailwind.

Finally, while inflation is definitely a concern, you have to realize that inflation is personal. While you definitely have to be aware that health care costs typically increase at a rate higher than general inflation (although Medicare helps a lot with this), as a retiree you are not as exposed to the rest of the inflation “basket” as younger, working folks. You typically don’t have to worry very much about inflation in housing costs, the price of vehicles, child care or college tuition. Your inflation (with the exception of medical costs) will likely be lower than the general rate of inflation. And while inflation in medical costs will offset that somewhat, many folks end up “double-counting” that, including it in both their insurance premiums/medical costs worries as described above and in the inflation worry bucket. You definitely should account for this, but you shouldn’t count it twice.

None of this is meant to imply that “everyone can retire now, it’ll be fine!” But I think it’s important when doing your own planning and calculations that you include these likely tailwinds and give them just as much emphasis as all of the possible negative events. Bad things do happen, but so do good things; don’t let the worst possible outcome be your base case.