A topic that frequently comes up in my financial literacy class for educators as well as just in general conversation is how to pay for potential long-term care costs in retirement. I want to be clear, I am in no way an expert on this topic. Having said that, I have done a fair amount of research into it and feel like I have some information that might be helpful for others. So below are some resources for you as well as my general thoughts on the topic.

Resources

These four resources are a great place to start.

- Long-Term Care Insurance NOW!: This is a free e-book (pdf) or you can purchase it at Amazon. This book is an excellent overview of the topic, including who long-term care insurance might be appropriate for and who it is not appropriate for. It also describes the various forms of long-term care insurance available in the market.

- Do You Really Need Long-Term Care Insurance?: This video from Erin Talks Money “breaks down what long-term care actually costs, how often retirees really need it, and the three most common ways middle-class and wealthy households plan for it — using real data, not fear-based assumptions.”

- 2025 Milliman Long-Term Care Index: This white paper “measures lifetime costs of formal paid LTC services for a 65-year-old in 2025 and accounts for the fact that not every person will require LTC.” Note that the Milliman figures assume all care is paid care when, in reality, families often provide free care for a certain amount of time, particularly when needs are less serious.

- How Much Will Your Long-Term Care Needs Cost?: This post from the Center for Retirement Research at Boston College is a nice, brief summary of the Milliman White Paper.

My Thoughts

There are quite a few unknowns when planning for retirement. The one that tends to worry people the most is the possibility of needing long-term care (LTC). This is a dual-edged worry. First, people are worried because they fear losing their physical and/or cognitive abilities and that they won’t be able to live the life they want to live. Second, people are worried that if they need help with physical or cognitive needs (or both) that it could be very costly to pay for that help. There’s not a lot I can say about the first worry, other than do everything possible to set yourself up for success by being as healthy as possible. This includes the boring but very important advice to eat well, exercise, and take any appropriate medications to treat conditions you do have to hopefully keep them from impacting your health even more.

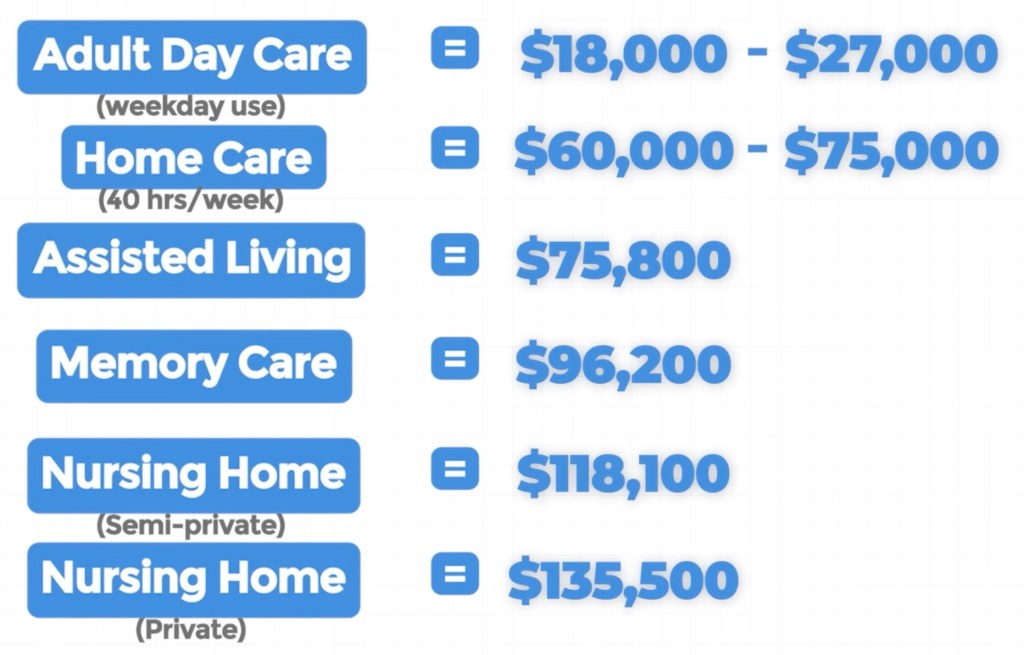

This post is about the second worry, addressing how to pay for the potential costs of long-term care. And, to be clear, these costs can be considerable. As a personal example, my mother is currently in Assisted Living here in Colorado and is paying about $8,900/month for a relatively low level of care need (it would cost more than that if and when she needs additional levels of care). For folks who progress beyond Assisted Living and need Memory Care, prices in the Denver metro area tend to start around $10,000/month and up. And nursing home care can be even more expensive. (Prices do vary tremendously both by location and by quality of the facility.)

The way we usually try to address outsized risks like this is insurance. Unfortunately, health insurance (including Medicare) does not pay for long-term care. You may be able to purchase long-term care insurance (LTCi) but, unlike health insurance and Medicare, you are not guaranteed to qualify for long-term care insurance. And if you do qualify, long-term care insurance is very expensive (and doesn’t necessarily cover all of the costs). How expensive varies, of course, but many people should expect to pay at least several thousands of dollars a month in premiums, and you will need to pay those premiums for many years before possibly needing to use the insurance. Again, it varies, but the ideal time to purchase long-term care insurance for many folks is in their mid 50’s, both because that’s when they are more likely to qualify and because the premiums will be lower if they start at a younger age. While the premiums are lower if you start younger, premiums can – and do – increase from year to year, although there are regulations in place for most LTCi policies that place restrictions on the amount of increases insurance companies are allowed to make.

I would encourage you to explore the resources listed above (and more), but here some of my main takeaways.

Three Levels of Wealth

As I mentioned previously, not everyone will qualify for long-term care insurance. If you don’t, then this section is moot, it won’t be an option for you. But for those who do, the question arises of whether they should. Because LTCi will cost a significant amount, and you may not get any return on investment for that cost (if you don’t need long-term care), then evaluating whether it is worth it for you is extremely important. For me, there are three levels of wealth to think about when considering whether to get LTCi (assuming you qualify).

- Low Level of Wealth (~less than $1 million): For folks with a small level of wealth, it probably doesn’t make sense to consider LTCi because it will be difficult to afford the premiums without impacting your lifestyle. In addition, you don’t have a lot of wealth to “protect” from the potential cost of long-term care. For folks in this category, the likely scenario is that if they need significant and costly long-term care they will spend down any remaining assets that they have and then Medicaid will pay for LTC. It’s important to keep in mind that many long-term care facilities don’t accept Medicaid and the ones that do are often not as nice, but there will be a care option available to you when the money runs out.

- High Level of Wealth (~more than $5 million): For these folks, LTCi likely doesn’t make sense because they can just self-insure. Even if they have significant long-term care costs they are not only unlikely to run out of money, but they will likely only draw down their wealth by a small amount because of the on-going investment gains from their wealth.

- Moderately Wealthy (~$1 million to $5 million): These are the folks who want to seriously consider LTCi. They have enough wealth that they likely want to protect it (for a spouse or to leave as a legacy), but not enough wealth that it can sustain long-term care spending indefinitely. Obviously there is quite the range between $1 million and $5 million, so everyone will have to decide their definition of what level of wealth is necessary to protect and how much is enough to not worry about it anymore.

We are currently in the moderately wealthy group, so what are we doing? Well, we looked into LTCi… and did not qualify because of some very minor prior medical issues (Scott, the author of LTCi NOW and an LTCi insurance broker, was very surprised we were denied for those issues). Now, to be clear, Scott thinks we likely could have shopped around and qualified for a slightly different policy than the one he recommended and we tried to get. But ultimately we decided to self-insure (which I’ll discuss more below).

What Are the Odds?

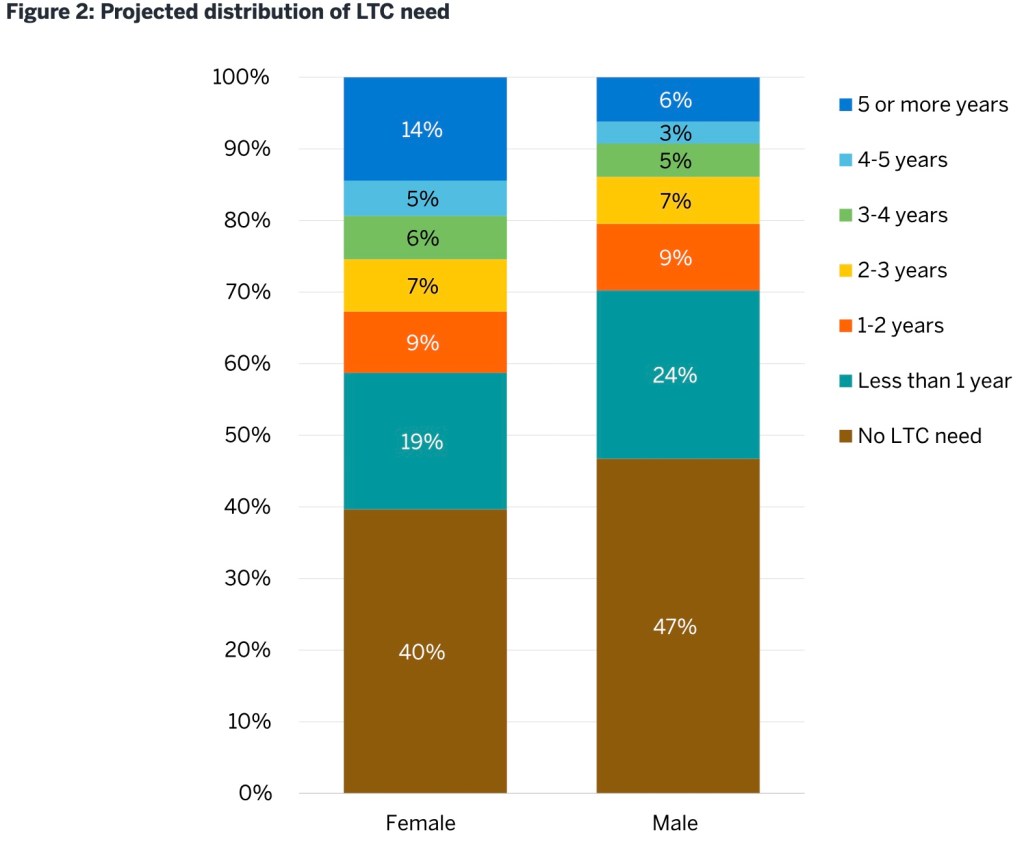

Erin’s video does a good job of providing some context around the data but, unfortunately, I’ve been unable to find the sources for her data. They do differ a bit from the Milliman numbers (not significantly, but enough that she must be getting them from somewhere else). So I’ll use the Milliman numbers for this since I have the source (but I do think the video is helpful for thinking through how to think about the numbers).

The first thing to notice about this chart is that women have an increased need for long-term care; that’s a function of the fact that they live longer. The second thing to notice is that needing LTC for a long period of time is really a tail risk, it’s not going to apply to a lot of folks. Borrowing from the way Erin framed similar numbers, out of 100 people:

- Approximately 43 (averaged male and female) will never need LTC

- Approximately 43 will need less than 4 years of LTC

- Approximately 14 will need 4 or more years of LTC

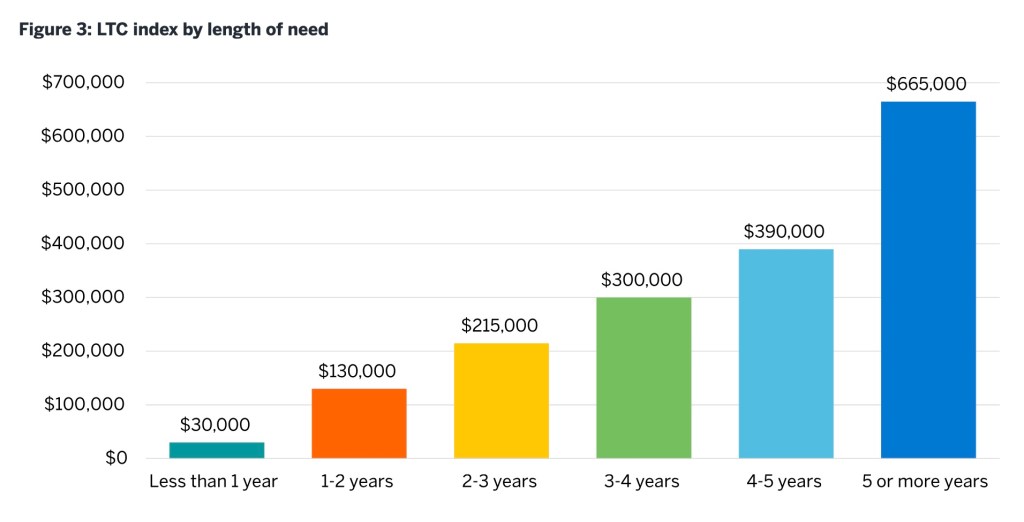

When you translate that into total cost (per person), that looks like this.

Again, using Erin’s framing, out of 100 people:

- Approximately 43 will spend $0 on LTC costs

- Approximately 43 will spend between $0 and $300,000 on LTC costs

- Approximately 14 will spend more than $300,000

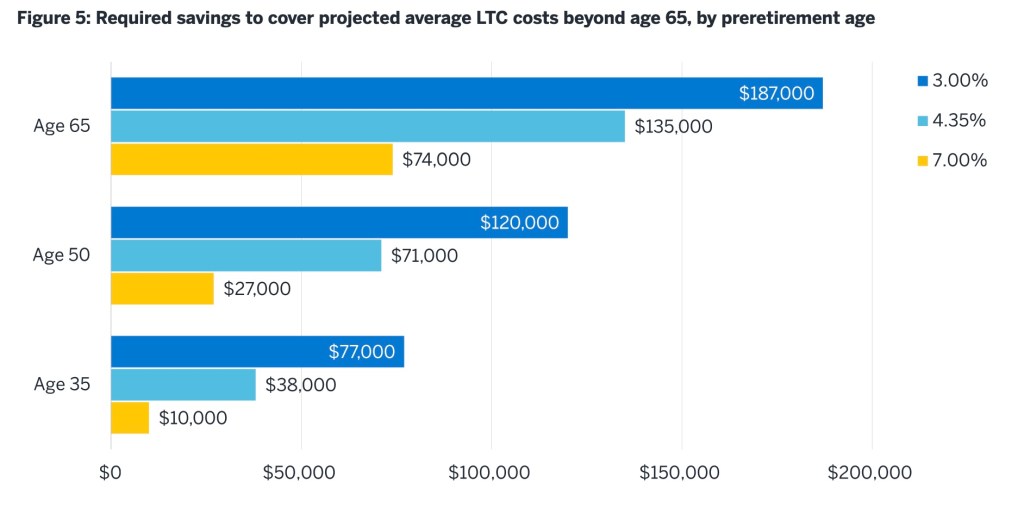

It’s only that last category that falls into the potentially catastrophic category, particularly if you have a partner and you both are unlucky enough to fall into that ~14%. Now 14%, while statistically unlikely, is still a number to be concerned with, so let’s think of tht in terms of someone in the “moderately wealthy” category. First, they likely have some kind of income coming in (Social Security and/or pension). Second, their assets will typically be growing over time as well. Milliman helpfully provides this chart for how much you need saved by age 65 to cover “average costs” with various assumed rates of return.

To be clear, I don’t want to minimize the potential impact of these high costs over multiple years. They certainly can be significant and negatively impact your lifestyle in retirement (particularly in the “low level of wealth” category) and the size of any legacy you leave. But for those in the moderately wealthy or high level of wealth categories, this is likely manageable (even if it is not desired).

Why Did We Choose To Self-Insure?

I mentioned above that we looked at LTCi, were denied on our first attempt, and then decided not to pursue different policies and just self-insure. To be clear, everyone’s situation is unique, as is their risk tolerances and their values around things like LTC and leaving a legacy. In our case, we have a decent amount of wealth, but perhaps not enough to completely self-insure as described above. But we also both have really good defined benefit pensions, which would go a long way toward paying long-term care costs out of our current “income”, meaning we wouldn’t necessarily need to draw down our assets by a significant amount each year. Given the expected growth of assets over time, we are likely in good shape unless both of us end up needing long-term care for an extended period of time and future market returns are less than they have been historically. For us, that seems like a reasonable way to go (especially when you consider the investment returns from the money that would’ve been spent on LTCi premiums from our late 50s on).

Does all this mean that I think LTCi is a bad idea? Absolutely not. If you have enough assets that you want to protect and/or you don’t want to end up in a facility that accepts Medicaid, then it can be a very good option. In addition, it’s important not to underestimate the “permission” factor that having LTCi gives you. Many people end up caring for loved ones far beyond the point that it’s healthy (for the loved one and for the caregiver). For folks who have LTCi, it tends to give them “permission” to allow others to help because they aren’t as worried about the cost. But you do have to be ready for the reality that you may not get approved and, if you do, you may be paying high (and increasing) premiums for the rest of your life.

Hopefully this post gave you some helpful resources and things to consider, but you’ll likely want to explore further on your own.