Correction 1-21-23: The original version of this post contained a mistake. The credit rate (50%, 20%, 10%) only applies to the first $2,000 you contribute to a qualified plan. Amounts above $2,000 don’t get the credit. In the original post, I assumed that as long as the credit rate times the amount contributed didn’t exceed $1,000, you would get the full amount. For example, 10% of a $4,000 contribution would be $400. But the amount that the credit is based on is capped at $2,000, so the most that a person with a 10% credit rate could get even if they contribute more than $2,000 is still $200. I apologize for the mistake.

For the majority of folks, taxes should be pretty simple these days. You’re most likely going to take the standard deduction at the federal level, so the only things to think about are ways to minimize your taxable income and occasionally to take advantage of special tax incentives. One of those incentives that is often overlooked is the Retirement Savings Contributions Credit (Saver’s Credit). The reason it’s often overlooked is that it has an income limit to claim it that is fairly low, so many folks make too much to claim it.

But many teachers at the beginning of their career are likely to qualify for this credit if they are able to put at least a little bit of money into a traditional, pre-tax retirement account (IRA, 401k, 403b, 457). This depends, of course, on a variety of factors, including how much they make, how much they contribute to their pension plan and pay in health/dental/vision premiums, and whether they have the ability to still pay the bills if they make a contribution to their retirement account. (As an aside, if you are a parent of a young teacher, this might be a way you could help out by providing the amount of their contribution that they would then use to pay the bills.) (Usual disclaimer: I am not a CPA, this is not specific tax advice, blah, blah, blah.)

Note: You can’t claim this credit if you are under age 18, claimed as a dependent on someone else’s taxes, or were a full-time student for five calendar months. That last one, especially, could apply to a teacher who graduates in the spring and then starts teaching that fall. They would be ineligible for the credit during that tax year, but then would be eligible the following year.

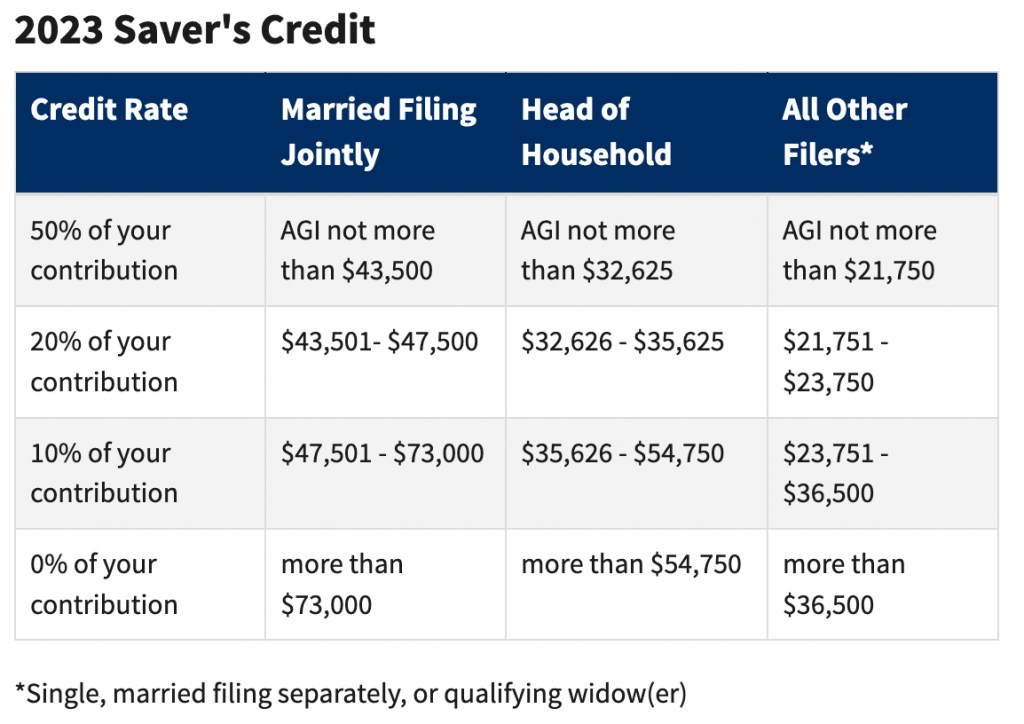

Let me give an example from my former district, Littleton Public Schools, here in Colorado. Littleton has one of the highest salary schedules (perhaps the highest) in the state, so this is the “worst case” scenario in the sense that it is going to be hardest to qualify for the Saver’s Credit due to the higher income. (For folks in Colorado districts who pay less, it will be easier to qualify.) If you take a look at the salary schedule, you’ll see that a first year teacher in LPS with a Bachelor’s degree will make $43,559. At first glance, that seems to disqualify them from the Saver’s Credit, because it’s over $36,500 for a single filer (for this post, I’m just going to assume the teacher is single). But that’s misleading, because the income limits for the Saver’s Credit are based on Adjusted Gross Income (AGI), not gross income, so let’s dive a little deeper.

Colorado teachers currently contribute 11% to their pension plan, and that contribution is pre-tax. So that subtracts $4,791 from their income making their AGI $38,768. Still too high. But we’re not done yet.

The premiums this teacher pays for health, dental and vision insurance also come out pre-tax. If you take the least expensive options for health, dental and vision, that’s an additional $777 that comes out pre-tax, taking their AGI to $37,991. (And, if they choose more expensive options, it would be even lower.) Still too high, as we need to be under $36,500.

But it’s important to realize that any contribution they make to a traditional, pre-tax retirement account (IRA, 401k, 403b, 457) will also lower their AGI. Colorado teachers have access to an excellent 401k plan, so if this teacher can contribute at least $1,491 to their 401k (or any pre-tax plan), they’ll qualify for the Saver’s Credit and get a $149.10 tax credit. Some folks will look at that amount and say, “Big Deal!”, but realize that’s an automatic 10% return on investment and it allows this first year teacher to start their retirement savings right away and let compound interest do its magic. Also keep in mind that it’s lowering their federal and state income tax as well. This teacher would be in the 12% federal bracket and Colorado has a flat tax rate of 4.4%, so a combined 16.4% tax break ($244.52 on a $1,491 contribution).

If the teacher can manage to bump their contribution up to $2,000, they’ll get a $200 credit (and save $328 on taxes). If they can contribute more than $2,000, the credit is still capped at $200 (10% of a maximum contribution of $2,000 that qualifies for the credit). Again, this teacher has to be able to pay the bills, so they will have to determine how much they can afford to contribute (unless, again, they have a parent who might be willing to help out with a “match”). But $1,491 equates to about $125 a month (about $104 after tax withholding savings, and about $92 if you pro-rate the tax credit), which is not an unreasonable amount to try to set aside.

It is likely that this teacher may be able to claim this credit for a couple of more years as well. Again, using LPS’s salary schedule (and today’s dollars, both in terms of the salary schedule and the Saver’s Credit limits), in their second year they will make $45,517, which would equate into a minimum contribution to their pre-tax retirement account of $3,234 in order to qualify (which would then get them a tax credit of $200). In their third year, they make $47,567, which would mean their contribution would have to rise to $5,058 to stay under the limit, which would get them a tax credit of $200.

After about year three it gets much tougher, both because their salary continues to increase as they move up steps on the salary schedule and because they likely will be moving horizontally across the schedule with continuing education. It may still be possible if they are really good savers or, conceivably, if they get married and their spouse has a relatively low income, but this generally will be an opportunity that most teachers will want to take a look at in the first two to three years.

Depending on where you live and work, of course, your salary schedule will be different. In some states, teacher salaries are much higher and it will be more difficult to qualify. In other states (and in other districts in Colorado), salaries are much lower, so it will be easier to qualify. But if you know anyone who is just starting to teach (or any career that has a low starting salary), have them take a look and see if they might be able to take advantage of this often overlooked tax credit.

Note: As part of the recent Appropriations Act, the Saver’s Credit will be changing to the Saver’s Match in 2027. This will change it from a tax credit to a match into your retirement account and it will also change the phase out amounts, but it will be fairly similar. For tax years until then, the Saver’s Credit is still in effect (and the income limits will get adjusted each year for inflation).

Addendum: Just to be clear, you can also get the Saver’s Credit for contributions to Roth accounts. I only used traditional, pre-tax accounts in the example in order to get below the income limit. But, once you are below that limit, Roth contributions would work as well.

One thought on “Saver’s Credit: An Overlooked Tax Credit for Many Beginning Teachers”