This post is mostly for me, as I need a place to refer folks to in the financial literacy for teachers class I teach for basic questions about taxes (and perhaps it could be useful for others as well). While there are a plethora of resources about taxes out there, I needed something that just covers the basics for the person who knows very little about taxes just to provide context for various discussions. Before we get started, some caveats.

- I’m not a CPA or tax attorney. This is not tax advice blah blah blah…

- The right tax moves for each person varies due to their individual circumstances, so this post may not have all the information necessary for your particular situation.

- Tax laws can change, and each state has its own tax laws. This post is designed to just cover the basics of taxes that are broadly applicable to teachers and, where it talks about state-specific topics, it applies to Colorado teachers.

- I will not talk about income earned from a business.

- This will be a very simplified explanation of how taxes work, please keep that in mind and don’t wonder why I didn’t get into more complicated topics.

Income and Deductions

Both your Federal and your Colorado state income taxes are based on your income, which seems simple enough but turns out to be somewhat more complicated. You start by adding up the income you receive from your job(s). As a teacher, you can add up your gross income from each of your paychecks (monthly for most teachers in Colorado). If you work any other jobs you could add that to your total as well. (Again, we aren’t going to go into the details of what happens if you also earn business income.) That may seem straightforward enough but, interestingly, that’s rarely a number you will actually put (or even see) on your tax return.

Instead, your employer(s) will send you a W-2 form in January and, in Box 1, labeled “Wages, tips, other comp”, you’ll see a number that for most people (and definitely Colorado teachers) will be less than the total amount you made for the year. (Note: The exact placement of the boxes can vary depending on your particular W-2.)

The reason for that is pre-tax deductions that your employer already knows about and therefore doesn’t report to the federal government as taxable income (and therefore doesn’t show up in Box 1 on your W-2). Here are the most common ones:

- Your Pension Contribution: Colorado teachers currently contribute 11% of their pay to Colorado PERA, which comes out pre-tax, so you will not pay federal (or state) tax on this now. (You will pay tax on it when you receive your pension in retirement.)

- Pre-Tax Insurance Premiums: Premiums that you pay for medical, dental and vision insurance can (and usually should) come out pre-tax. (If your PERA membership date is prior to June 30, 2019, this also comes out pre-PERA, which is even more savings.) (more info)

- Dependent Care Spending Account: If you have children in daycare, you can (and usually should) have that contribution come out pre-tax as well (2023 limit is $5,000). (If your PERA membership date is prior to June 30, 2019, this also comes out pre-PERA, which is even more savings.)

- Flexible Spending Account (FSA): If your employer offers certain health insurance options that are not HSA-qualified (more on that in a minute), then they likely offer an FSA, which allows you to set aside pre-tax money for any out-of-pocket medical, dental or vision expenses you pay during the year. (2023 limit is $3,050, can be spent on anyone in your family.) You generally have to spend this money each year or “lose it,” although your employer can allow you to carryover up to $610 (2023) to the next year if they choose.(If your PERA membership date is prior to June 30, 2019, this also comes out pre-PERA, which is even more savings.) (more info)

- Health Savings Account (HSA): If your employer offers certain health insurance options that are HSA-qualified High Deductible Health Plans (and you choose one of these plans), you can set-aside pre-tax money for medical, dental and vision insurance just like with the FSA. Unlike the FSA, however, the money is yours and you can carry it over from year to year or even move to a different HSA account in your name elsewhere. You can also usually invest this money, which opens up some intriguing possibilities. (2023 limit is $3,850 self/$7,750 family, with an additional $1,000 catch-up contribution for those over age 55.) Many employers also contribute some money to your HSA for you (that limit includes employer contributions).

- Limited Purpose Flexible Spending Account: If your employer offers HSA-qualified plans, they may also offer a Limited Purpose HSA. This is additional (to the HSA) pre-tax money you can set aside that can only be spent on dental and vision (not medical) each year. (2023 limit: $3,050). Like the regular FSA, this is use it or lose it. (If your PERA membership date is prior to June 30, 2019, this also comes out pre-PERA, which is even more savings.)

- Transportation Benefit Exclusion: This one is more rare, but if your employer offers it you can set aside up to $300 per year for transit passes and van pool services and/or $300 per year for parking expenses. (If your PERA membership date is prior to June 30, 2019, this also comes out pre-PERA, which is even more savings.)

- Optional Retirement Plan Contributions: If you contribute to a pre-tax 401k, 403b or 457b through your employer, this will also come out pre-tax and therefore not be reflected in Box 1 of your W-2. (more info)

So your W-2 will already reflect those deductions from your total income so it won’t get reported on your federal tax form. But there are also many other pre-tax deductions that you can take that your employer doesn’t know about. There are way too many of these to try to discuss them all, but here are some of the most common that apply to teachers.

- Traditional IRA Contribution: If you contribute to a traditional, pre-tax IRA you can deduct this amount as well (in addition to any 401k/403b/457b contributions, income limits apply).

- Educator Expense Deduction: If you spend your own money on classroom supplies, you can deduct up to $300 (2023) from your income ($600 if both spouses are educators).

- Other HSA Contributions: Even if you contribute to your HSA through your employer, it’s possible that you didn’t max out your contributions through your employer. You are allowed to “manually” contribute to your HSA (as long as you are within the limit), and those can be deducted as well.

You may also have some additional income that you have to add in, typically interest on savings accounts and perhaps dividends and/or capital gains from your investments. Interest is pretty straightforward, it just gets added to your income. Dividends and capital gains are a bit trickier (we’ll talk about them more below), but just realize that they will factor into the taxes you owe. (And, don’t sweat it, you have software that helps you figure out how to do this.)

So when you add up all your income and subtract all your deductions (to this point), you come up with something called Adjusted Gross Income (AGI) (line 11 on federal form 1040). But, even now, this is not what you get taxed on. Because now you get to take additional deductions. A small number of folks (particularly in Colorado) will be able to itemize deductions, which is beyond the scope of this post. But most folks (more than 90%) will end up taking the standard deduction (In 2023, $13,850 for single, $27,700 for married filing jointly, $20,800 for head of household (with additional deductions if you are over 65 or blind).

When you now subtract the standard deduction (or itemized deduction), you come up with your taxable income (line 15 on 1040).

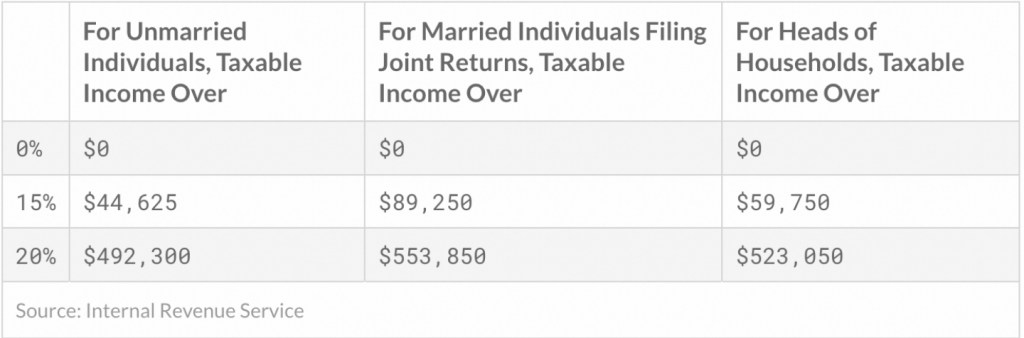

Calculating Taxes Owed (Income Tax Brackets)

Our federal tax system is what’s known as a progressive system, meaning the amount and percentage of taxes you pay changes (increases) with your taxable income. (Colorado has a flat state income tax of 4.25%). In 2023, this is what the federal tax brackets look like.

An important thing to keep in mind is that the tax bracket you are in is your marginal tax rate, but is not your effective tax rate. For example, if you are married filing jointly and your taxable income is $90,000, then you are in the 22% marginal tax bracket, which means that the last dollar you earned is taxed at 22% at the federal level. But that doesn’t mean all of your income is taxed at 22%. The first $22,000 is taxed at 10% (so you owe $2,200 in taxes on that part), the next $77,450 (from $22,000 to $89,450) is taxed at 12% (so an additional $9,294 in taxes owed), and the last $550 (from $89,450 up to your $90,000 taxable income) is taxed at 22% (so an additional $121 in taxes owed). Which means you owe (at this point, more to come) a total of $11,615 in taxes ($2,200 + $9,294 + $121), which works out to an effective tax rate of 12.9%.

Dividends and Capital Gains Taxes

If you have taxable investments (not savings-type accounts which earn interest, but brokerage-type accounts that can earn dividends or capital gains), these are taxed at a different percentage than ordinary earned income. This is what the capital gains tax brackets look like for 2023:

Not to go into too much detail, but some dividends and short-term capital gains (investments held less than a year) are taxed at ordinary income rates (the preceding section). But qualified dividends and long-term capital gains are taxed at either 0%, 15% or 20% depending on your taxable income (which, remember, includes dividends and capital gains). In our example with a taxable income of $90,000 for a married couple filing jointly (that number includes any qualified dividends and long-term capital gains), then only up to the first $750 in qualified dividends or long-term capital gains would be taxed at 15% (instead of your marginal tax rate of 22%), and the rest of your qualified dividends or capital gains would actually be taxed at 0%. Their ordinary income (taxable income less the qualified dividends and long-term capital gains) would still be taxed according to the tables in the preceding section. (Again, don’t worry, your tax software will do this all for you as long as you enter the numbers correctly.)

At this point, you have how much total tax you owe…well, sort of (line 16 of 1040). Because now you frequently have tax credits.

Tax Credits

Unlike tax deductions (above) which lower your taxable income, tax credits actually lower how much tax you owe dollar-for-dollar (so, dollar-for-dollar, tax credits are better than tax deductions). Again, there are many, many, many possible tax credits, we will just list some of the most common ones for teachers:

- Child Tax Credit: If you have dependent kids under age 17, you can receive up to a $2,000 tax credit for each of them (there are income limits for this that phase out the credit).

- EV and Energy Tax Credits: There are tax credits you can sometimes receive if you’ve purchased a qualified electric vehicle, solar panels, or made other energy-efficient improvements to your home. (more info and even more info).

- Saver’s Credit: In a teacher’s first year or two, they may qualify for the Saver’s Credit.

- American Opportunity or Lifetime Learning Tax Credit: Tax credits you may receive for paying for undergraduate or continuing higher education.

- Additional Dependent Care Expenses Tax Credit: Even if you contribute to a Dependent Care Spending Account (above) through your employer, you may (and likely will) have additional expenses above and beyond the $5,000. A portion of these expenses can be used as a tax credit.

The total of these credits are then subtracted from the total tax you owed on line 16, giving you your actual total tax owed (line 24).

Taxes Withheld and Due

You have both federal and state (and sometimes local) taxes withheld from your paycheck. You total up all the taxes withheld (Box 2 on your W-2 for federal taxes withheld). The difference between what you have withheld and what you owe is either your refund (if you have more withheld than you owe, line 34) or your payment due (if you had less withheld, line 37).

Colorado State Income Taxes

State income taxes in Colorado are fairly straightforward. While there are quite a few deductions, credits, and other things that can complicate it, for the most part you simply take your taxable income from your federal return and put it on your Colorado return. Unlike federal taxes, Colorado has a flat 4.4% state income tax. Here are a couple of common things teachers should know about:

- 529 Plan Contributions: Contributions to Colorado’s 529 plan come out pre-tax for your state income taxes (and there are even some matching funds available).

- Social Security Income: If you are at least age 65, then Social Security income is not taxed by Colorado.

- Other Retirement Income: If you are at least age 55, then up to $20,000 of retirement income (Social Security, pension, IRA distributions) is exempt from Colorado state taxes. At age 65, that increases to $24,000.

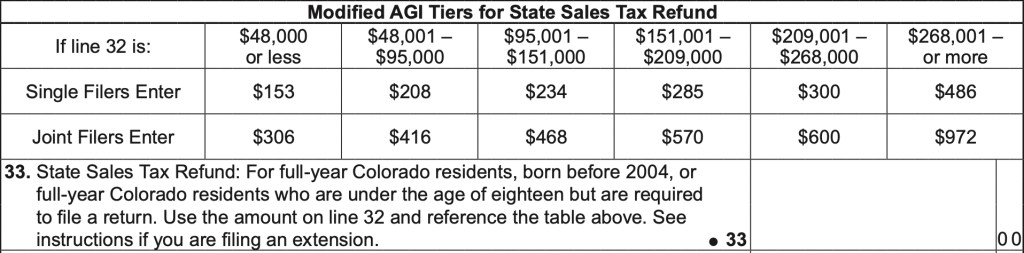

TABOR Refunds: Colorado has a constitutional amendment in place that limits state revenue. When revenue exceeds this limit, taxpayers receive a “refund” of this amount which effectively lowers the amount of state taxes you pay (technically it’s a sales tax refund). Even though Colorado’s tax rate is flat, TABOR refunds are often progressive. Here’s 2022’s:

Retirement Accounts: Traditional and Roth

I talked above about pre-tax contributions to traditional 401ks, 403bs, 457bs and IRAs. But there is also a Roth version of each of these accounts where contributions are not pre-tax (but withdrawals are). Please see this post for more on these types of accounts but, briefly, here are some considerations on whether it’s better to do traditional (pre-tax) or Roth (post-tax).

- Traditional Pre-Tax: Lowers the taxes you pay now, but you’ll pay taxes when you withdraw the funds in retirement. You get the “extra” money now by not paying taxes on your contributions, and the tax break you get is generally at your marginal tax rate (not your effective tax rate). You also know for sure what tax break you are getting because you know for sure what your tax rate is now. The downside is that you don’t know what your tax rate will be when you withdraw the money in retirement, both because you don’t know what your taxable income will be then and because the tax laws can (and will) change between now and then. This also means that you don’t know the true total value in your account because some of the balance will go to taxes, not to you.

- Roth: You pay taxes now, but don’t pay when you withdraw in retirement. You don’t get the “extra” now, but you know exactly what you will get when you withdraw because there will be no taxes due. But it’s possible that the tax rate you pay now on the contributions will be higher than the tax rate (and total taxes) you will “save” when you withdraw.

- Taxable Brokerage Account: While not a “retirement account”, it does still have tax advantages (qualified dividends and long-term capital gains are taxed at a rate lower than ordinary income). This can be used as part of your retirement investment portfolio.

Student Loan Repayments: While not explicitly part of filing your taxes, income-based student loan repayment plans are based on AGI. So anything that lowers your AGI (like traditional contributions) may end up lowering your student loan payments. Therefore, if you have federal student loans, there is likely an incentive to make traditional, pre-tax contributions (vs. Roth) at least during your first ten years (before PSLF hopefully kicks in for you).

Because career Colorado teachers will receive a good pension from PERA in retirement, and because that pension is taxable, most Colorado teachers will be in at least a “medium” tax bracket in retirement. This can be an argument for making at least some Roth contributions. (Again, if you have federal student loans and qualify for income-based repayment and PSLF, it might make sense for those Roth contributions to come after your first ten years where you are making pre-tax contributions in order to lower your student loan payment.) For most Colorado teachers, you will likely want to make some traditional and some Roth contributions over the course of your working career in order to provide flexibility in the tax impacts of withdrawals from these accounts in retirement.

Conclusion

So, again, this was meant to just be a basic overview of taxes for folks who don’t know much about them in order to help them make sense of other financial decisions (like contributing to retirement accounts). This in no way was meant to cover everything and, as I said, individual circumstances matter. But hopefully it will serve as a basic primer for some folks in my class (and perhaps for some other folks out there).

3 thoughts on “Taxes For Teachers 101”